By Lou Covey

Editorial Director

By Lou Covey

Editorial Director

As Semicon West approaches in two months, there will be a rising chorus of predictions for 450mm manufacturing and test equipment. But silicon wafer industry revenues are heading in the wrong direction, dramatic technology advances in test and reclamation, and an overall urge for revenge among their customers over gouging during the solar boom.

In February, SEMI issued its annual report on the state of silicon wafer industry that showed a small increase in the delivery of wafers to customers in spite of a well-known glut of supply, but a sharp decline in revenues that outstripped reasons based on inventory. What is more, this appears to be developing into a trend over the past three years.

When questioned about the discrepancy, SEMI replied simply, but cryptically, that it was due to "market pressures and a weak yen.” Yet placing the blame on the decline of Japanese currency seemed knee-jerkish at best. While it is true the yen has plummeted over the past 20 years, the decline has relatively flattened out over the past five years. Japan, while still the leading supplier, has seen a significant increase in competition worldwide especially in China, Malaysia and even the US, modifying the yen's influence even more. The extremely vague explanation "market pressures" is even more suspect. Let’s take a look at test, for example.

A joint study by Hewlett Packard, the University of Oregon and the University of California, San Diego showed that applying data mining to optimize IC test resulted in significantly higher yields on virgin wafers. At ITC in 2013, Craig Nishizaki, Senior Director of ATE Development at NVIDIA, extolled the benefits of test data management methodologies. Higher yield through improved test reduces demand. Although, you wouldn’t know it talking to people in the test management industry.

Jim Reedholm, an independent representative of Yieldwerx, based in Austin Texas. “I haven’t seen any data that would backup any claim that effective test management would reduce demand for wafers, but it sounds right.” Executives at other semiconductor test management technology companies were either unresponsive or, strangely enough, unlocatable.

OK, so maybe no, maybe yes. How about reclaimed wafers?

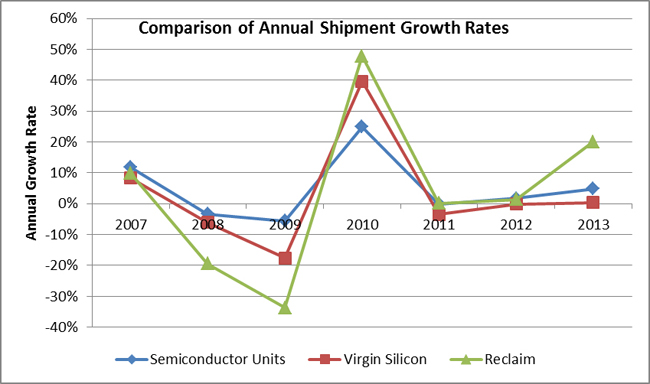

According to Semico analyst Joanne Ito, improvements in reclamation processes for silicon wafers has dramatically dropped the demand for test wafers for semiconductor manufacturing and, according to SEMI, both revenue and material shipments are up 14 percent from last year. Ito believes that will be a trend going forward, but SEMI predicts that increase will flatten out by 2015. We might be getting closer to a reason for the discrepancy between revenue and shipments.

According to Ito, during the solar boom up to 2008 there was a significant lack of raw material for wafers, which drove up prices for the high-quality virgin wafers that the semiconductor industry needs. That same solar demand ate up the capacity for 200mm and 300mm manufacturing. When the boom blew out, demand for the raw material dropped and a huge overcapacity developed in 200-300mm facilities.

OK, so oversupply tends to push down prices and revenues. Econ 101. There is only one problem. Demand has not decreased in the semi industry. It is increasing as demand for smart devices worldwide drives semi design starts. Hence, the steady increase in shipments to semi customers. Why the dramatic drop in revenue?

Ito thinks the answer might be vengeful purchasing executives in semiconductor companies.

“During the solar boom, the semi industry (which has higher requirements for the wafers than solar) saw an annual increase in prices of 10-12 percent from the wafer manufacturers because of the cost of silicon raw materials. So the semi industry said, ‘We paid you a when the cost went up, we want this cost reduction reflected in our prices.”

Now we have a better idea what “market pressures” are actually in play. The opportunity to return to the wafer manufacturers what they forced upon their customers a decade ago is too good to resist.

This quid pro quo may seem good for the industry in the short run. However, long-term it is causing significant problems. We will take a look at that next week…

Do you agree there is an element of vengeance going on, or do you see other factors at play? Leave a comment and tell us what you think.